As a business owner, one of the most important factors to ascertain is how many goods or services you need to sell to cover your expenses to become profitable. This accounting metric is known as the break-even point.

In previous articles, we have conveyed the importance of a business’s cash flow and developing a system around cash flow management. This is the cornerstone of running a successful business.

In this article, we are still concentrating on an organization’s revenue and expenses; however, we are simplifying the process down to one number. Let’s explore the intricacies of this number and how to model it for your business.

Understanding Break-Even Point

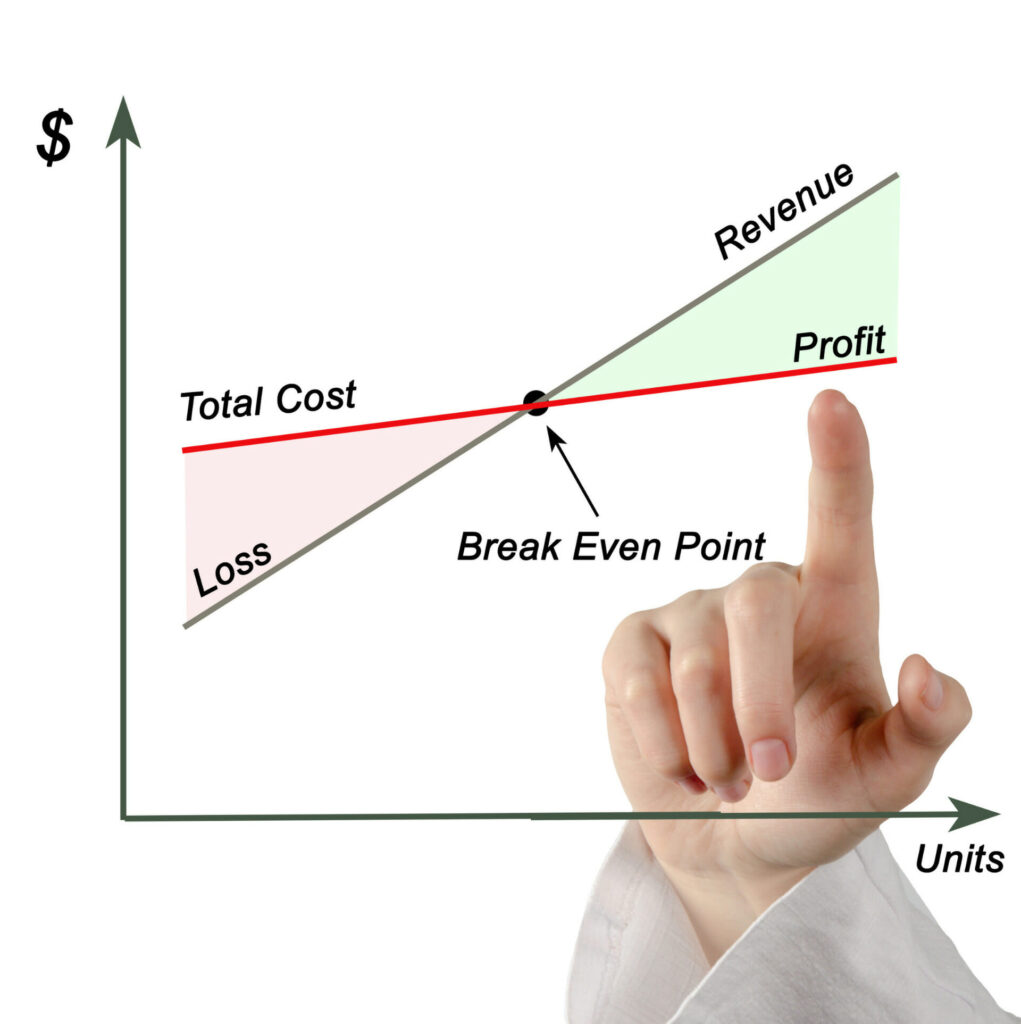

A company’s break-even point or break-even analysis is the point at which its sales equal the cost of doing business. The organization has not made a profit yet but is not operating at a loss.

Every product a company sells or service offers carries an associated cost. Whether it is the cost of the raw materials or wages to implement new software, there are always costs incurred when running a business.

These costs show up as the cost of goods sold (COGS) in a production environment. The more physical products you produce, the higher your COGS.

By understanding how much output is required for the company to break even, adjustments can be made accordingly. A business can adjust output as well as the sale price of their products or services.

Beyond the break-even point, all incremental revenue beyond this point contributes to the organization’s gross profit.

Break-Even Point Formula

A break-even analysis is a formula that shows how many units of phones, chairs, legal services, etc. you need to sell to cover your costs.

Calculating the break-even point involves taking the fixed cost and dividing the amount by the contribution margin per unit. To find the contribution margin per unit, take the price per unit and subtract the variable costs per unit.

Before calculating this formula, we need to pinpoint the following three variables.

1. Fixed Costs – these are costs independent of sales volumes, such as rent, insurance, and loan payments. These are commonly known as SG&A.

2. Variable Costs – are expenses that fluctuate up or down per sales volume. Examples are raw materials, manufacturing labor costs, and sales commissions, which are generally part of COGS.

3. The sale price of the product or service.

After you can establish these numbers, you can calculate the break-even point expressed in units produced or quantity of service sold.

Example

To illustrate the break-even point, let’s assume a sock manufacturer has fixed expenses that total $10,000 per month. Their variable cost (COGS) per unit is $5 per pair of socks, and the socks retail for $25 (sale price).

We first find the contribution margin, which is $20 per pair of socks. Then by dividing the fixed costs by the contribution margin, you will know how many units of socks you need to sell to break even.

Analysis

A break-even analysis is helpful whether you are just starting a business or have been operating already for several years. It is never too late to start using this new tool, and there are also a few instances where this metric becomes increasingly valuable.

◦ Before starting a business – it is essential to conduct this financial analysis when developing a business plan. Then you will have a good idea of the risks involved.

◦ New product or service – existing businesses should conduct this analysis before launching a new product to learn how it will affect profitability. You might discover you will need to sell too many units to cover your overhead.

◦ Performing a break-even point for a new product may help determine the right price for the item.

◦ Changes in manufacturing – a business is considering outsourcing a portion of their manufacturing. Suppose the organization can produce the same quality with a lower variable cost but isn’t sure if working with a partner would increase the fixed cost. In that case, this analysis will play a critical role in determining if the change would be cost-effective.

All businesses want to be as profitable as possible. Calculating the break-even point is just one component of cost analysis, but it is often an essential first step in establishing a retail price point that safeguards a profit.

Conducting a break-even analysis is a powerful tool for planning and decision-making. Performing this calculation on a long-term basis can identify critical information like price variability, setting appropriate sales targets, and highlighting weaknesses in the current business model.

How FINSYNC Can Help

FINSYNC allows you to run your business on One Platform. You can send and receive payments, process payroll, automate accounting, and manage cash flow. To learn more about how we can help your business start, scale, and succeed, contact us today.