There are several boxes to check after a business hires its first contracted employees or vendors. The W9 Form is one of the many tax documents required by the IRS to estimate the taxes owed by contract or freelance workers within a given year.

It is easy to push all tax-related tasks off until tax season as a business owner. However, the W9 Form is critical when paying for non-employee services, and failing to provide the 1099 form to vendors by the January 31st deadline can create risks for your organization.

This article will provide the purpose of a W9 form and how it differs from the 1099 tax form. We will also walk you through a checklist to ensure you have the information you need. Lastly, we will go over some items to keep an eye out for when collecting this information.

1099 Form

To understand the W9 Form, it is beneficial to have first-hand experience with 1099 forms.

Businesses file 1099 forms when they have paid more than $600 to an independent contractor or non-employee during the year. You do not need to withhold any money when you provide payment; however, you must use the 1099 form to declare the exact dollar amount your company disbursed to the IRS.

Therefore, the 1099 form serves as a record for the total amount of compensation a non-employee received. Before a contractor begins a work assignment, your business must deliver the W9 Form; then, the contractor must complete it before starting their project. This Form gives your business the necessary information to provide the 1099 form at the end of the tax period.

Purpose of W9 Form

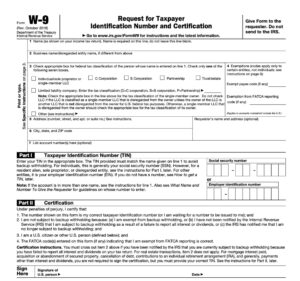

The W-9 Form, officially titled “Request for Taxpayer Identification Number and Certification,” is used to verify your independent contractor’s tax withholding status. They will supply you with their TIN or Tax Identification Number, which you use later in conjunction with the 1099 form.

Besides non-employee compensation, here are a few other examples of W9 income.

◦ Cancelation of debt

◦ Acquisition or abandonment of secured property

◦ Real estate transactions

◦ Mortgage interest

◦ Miscellaneous income

Blank W9 forms are found on the IRS website and can be downloaded and given to new contractors as part of the hiring process.

Checklist for Completing

Form W9 is one of the most straightforward IRS forms to complete.

Here are the required fields that all non-employed staff must complete.

Box 1: Contractor name goes here as it appears on their tax return.

Box 2 – Business name. Enter LLC, S-Corp, or sole proprietor name here.

Box 3: Box check required to distinguish between LLC, S-Corp, or sole proprietor.

Box 4 – Exemptions. Certain businesses are exempt from backup withholding, and this is when the employer is required to withhold a percentage of any future payments to ensure the IRS receives the tax due on this income.

Most likely, backup withholding will not apply unless a vendor refuses to provide a Social Security number (SSN) or tax identification number (TIN)

Box 5 – Business street address, city, state, and zip code.

Box 6 – Option box to include requestor’s name or payer’s name.

Box 7 – Social security number or tax identification number. If a business is a partnership, LLC, or corporation, there should already be a TIN, also referred to as an Employer Identification Number (EIN).

Box 8 – Signature required to attest to the truthfulness of all information.

Things to Look Out for

If you have a contractor who will not provide their completed W9 or TIN, the IRS requires your company to start withholding 24% of their compensation for tax money. There are penalties for failing to submit this backup withholding, and it is better to avoid this altogether and require W9 completion before work begins.

Since the W9 Form contains sensitive information, always make sure to use secure channels to send it. If your organization uses email for the hiring process, ensure the contractor sends the form back encrypted.

If a single person owns the LLC, list the name of the owner on the “name” line in box one and the name of the LLC on the “business name” line in box 2. If the business owner provides both SSN and TIN, the IRS would prefer the owner’s Social Security number.

At the end of the tax year, the information contained on the completed Form W9 gets used to prepare 1099 forms like 1099-NEC, 1099-MISC, 1099-INT, and 1099-DIV. Therefore, ensuring the W9 Form gets completed accurately will save you time during tax season.

How FINSYNC Can Help

FINSYNC allows you to run your business on One Platform. You can send and receive payments, process payroll, automate accounting, and manage cash flow. To learn more about how we can help your business start, scale, and succeed, contact us today.