Whether you’re launching a new business or have been operating for years, streamlining your accounting process is essential for maintaining efficiency and compliance. A powerful way to optimize efficiency is by implementing a payroll processing system. These platforms automate tasks like tracking employee hours, calculating wages, and managing tax deductions, significantly reducing administrative burdens. Many payroll systems also integrate with accounting software, helping to simplify your financial records and improve accuracy.

Thinking about upgrading your payroll process? Here’s what you need to know.

What Is a Payroll Processing System?

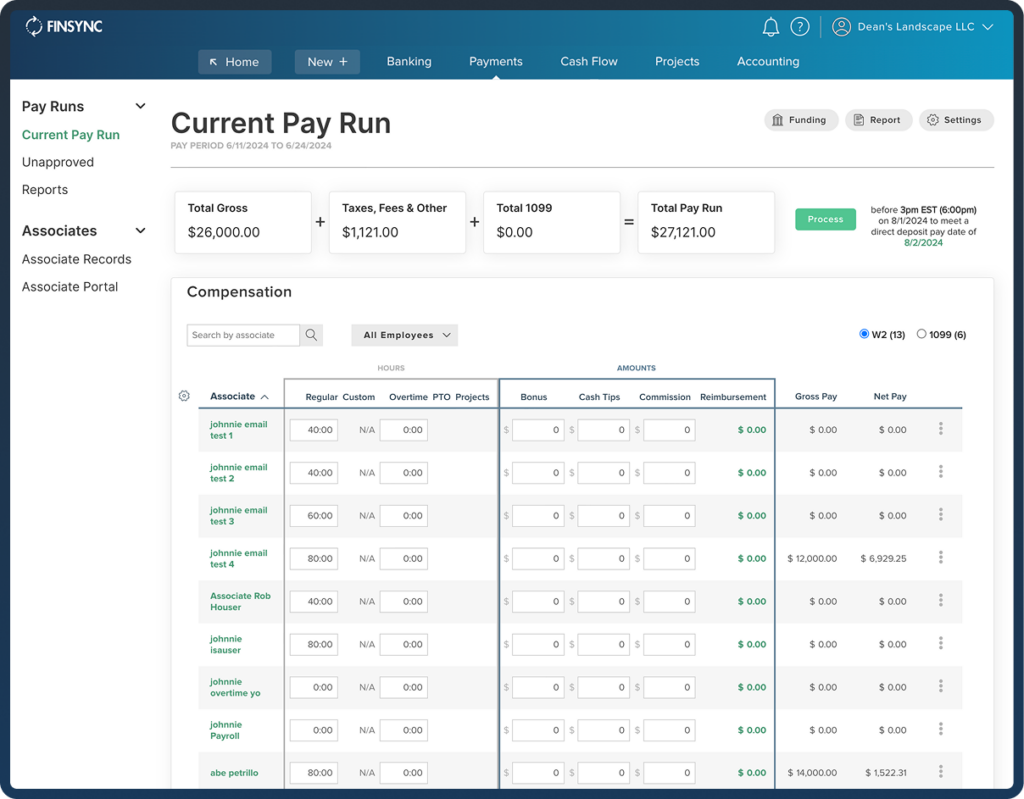

A payroll processing system is software that automates employee compensation tasks, from calculating paychecks to ensuring tax compliance. These systems handle everything from tracking hours worked to managing PTO, tax withholdings, and benefits deductions.

This software automates employee compensation by handling payroll calculations, generating pay stubs, and seamlessly processing direct deposits. Advanced systems even provide employees with access to secure self-service portals, where they can view pay stubs, W-2 forms, and other documents.

For businesses that prefer outsourcing, third-party providers offer payroll processing services. However, with the right system, businesses can easily maintain accurate payroll and ensure compliance without external help.

About FINSYNC Timekeeping App

Using a timekeeping app integrated with your payroll system is a powerful way to improve accuracy and efficiency. Employees can log their hours for specific tasks or projects, and managers can review and approve timesheets with ease. This process helps ensure that employees are paid accurately for their work, reducing payroll errors and preventing overpayments.

Moreover, some payroll systems provide automated reporting and analytics, offering businesses insights into employee time management, productivity, and labor costs, which enables better operational decisions.

Benefits of Using a Payroll System

Payroll processing systems provide numerous advantages for businesses of all sizes. Here are some key benefits:

- Automation: Reduce manual labor and accounting errors by automating tasks like calculating taxes, generating paychecks, and filing reports.

- Increased Efficiency: By automating repetitive tasks like wage calculations and report generation, payroll systems free up valuable time for HR and accounting teams to focus on more strategic business functions.

- Cost Savings: Payroll errors can be costly, whether from overpayments, tax miscalculations, or fines from non-compliance. Automated payroll systems reduce these risks by handling complex calculations with precision.

- Compliance Support: One of the most significant challenges with payroll is staying compliant with changing tax laws and employment regulations. Staying compliant with evolving tax regulations is easy when systems automatically update to reflect the latest laws and requirements.

- Employee satisfaction: A self-service system provides employees with easy access to their pay stubs, tax documents, and other payroll information.

As a result of payroll systems, companies can reduce operational costs and focus on strategic growth.

Choosing the Right System

Choosing the right payroll system is crucial as your business depends on it. Considering size, industry, and future growth potential, the ideal system should align with your company’s needs. Here are the key factors to weigh when choosing a payroll system:

Cloud-Based vs. On-Premise

One of the first decisions you must make is choosing between a cloud-based or an on-premise solution. Cloud-based payroll systems provide more flexibility as they allow remote access, making it easy for your team to manage payroll from anywhere with an internet connection. This option is handy for businesses with remote employees or multiple locations.

With built-in automatic updates, cloud-based systems ensure you stay compliant and up to date without lifting a finger.

On the flip side, on-premise payroll systems offer a different kind of advantage. They provide a high level of control and customization, which can be particularly beneficial for larger companies with specific security or regulatory requirements. While they may require more IT support and maintenance, the level of control they offer can make you feel empowered and in charge of your payroll operations.

Scalability

As your business grows, so do your payroll needs. Choosing a payroll system that can scale alongside your company is essential. This means finding a system that can easily add new employees and locations or even expand to accommodate multi-state or international payroll if necessary.

Many payroll solutions integrate seamlessly with other HR and accounting tools, which can be invaluable as your company’s operations become more complex. Scalability ensures that you won’t have to switch systems or face disruptions as your business evolves.

Direct Deposit and Tax Filing

Modern payroll systems should support direct deposit, allowing employees to receive their pay quickly and efficiently. This feature eliminates the need for paper checks and manual processing, saving significant time and reducing the risk of errors.

Additionally, a robust payroll system should handle automatic tax calculations and filings. This includes keeping up with the latest federal, state, and local tax rates, calculating withholdings, and submitting payroll tax forms on time.

By automating these processes, you not only reduce errors but also ensure compliance with tax laws, minimizing the risk of fines and penalties. This automation can provide a sense of relief, knowing that these crucial tasks are being handled efficiently.

By considering these factors, you can select the right payroll system to meet your business needs today and support your growth in the future.

Challenges of Implementing Payroll Processing

Adopting a new payroll system comes with challenges: tracking employee absences, navigating tax law changes, and ensuring compliance with wage regulations.

To address these issues, it is critical to:

• Stay Updated on Tax Laws: Payroll involves complex tax calculations, and tax laws can change frequently at federal, state, and local levels. Payroll software can automatically update tax rates and ensure compliance which helps avoid costly penalties associated with late or inaccurate tax filings.

• Managing Employee Absences: When employees take time off, it’s crucial to track these hours accurately to avoid payroll errors. Without proper tools, managing absences can lead to discrepancies in pay, overtime miscalculations, and compliance issues.

• Ensure Employee Data Security: Payroll systems handle highly sensitive employee information, including Social Security numbers, bank account details, and personal identification. Protecting this data is paramount to avoid data breaches and comply with regulations such as GDPR or HIPAA, depending on the region.

Conclusion

Implementing a payroll processing system can be challenging. You will need to train employees on how to use the platform and ensure that it meets all government requirements.

Yes, implementation takes effort, but the time and cost savings of a payroll system far outweigh the challenges. Having an automatic process can save you time and money by automating many of the tasks associated with payroll. Overall, a payroll processing system can help to streamline your accounting process and make your business run more smoothly.