Christophe Choquart followed his passion for art and opened LM Frame & Gallery in July of 2020 in Marietta, GA. We had the opportunity to interview him and learn more about his journey and how FINSYNC has helped him along the way.

Tell me about your company and what inspired you to start

I have been a collector of art for a while, and I’ve always had the idea of opening a gallery where I could display Australian art. I ended up having the opportunity to purchase my gallery in July of 2020, right in the middle of COVID. When I saw that the business that was previously located here was going to close, I decided to follow my passion and open LM Frame & Gallery. I was looking to diversify and create an ecosystem with an art shop that could be a one-stop shop for art and framing.

What are some of the challenges you’ve faced as a small business owner?

There have been many challenges! Due to COVID, we’ve experienced supply chain issues. It has been challenging to keep up with inventory and inflation. As a small business owner, there are always things that need to be fixed. You’re accountable for every single mistake while keeping everyone happy and managing your team. Sometimes, there are not enough hours in the day to get everything done.

What’s the best thing about being a small business owner?

Following my passion and making clients happy. To me, the greatest thing is working around art and helping people enhance their art with custom frames.

What prompted you to start using FINSYNC?

I had the opportunity to work with FINSYNC software at my previous job. I wanted to have a tool that would be a one-stop shop where I could pay my suppliers, do my payroll, monitor my P&L, check my bank information, and get bookkeeping help. FINSYNC has allowed me to have a clear understanding of my business and where I was heading.

What financial institutions do you have connected to FINSYNC?

I have Chase Bank, which is my main operating bank.

How does having FINSYNC connected to the accounts mentioned above make your business life easier?

I can very quickly categorize my spending. I have quick access to view my P&L, monitor cash flow, and make decisions based on cash flow scenarios. Having my accounts connected has helped me manage my cash flow and bookkeeping.

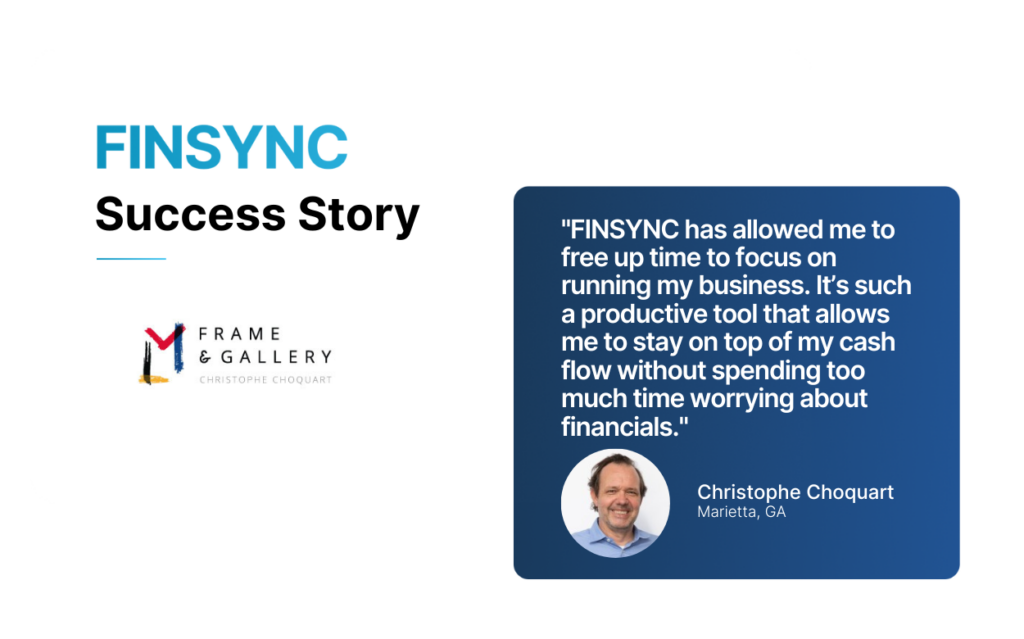

What are the biggest benefits your business has experienced using FINSYNC?

FINSYNC has allowed me to free up time to focus on running my business. I can go in at any time and see what is coming in and out. It’s such a productive tool that allows me to stay on top of my cash flow without spending too much time worrying about financials.

What advice do you have for those who are thinking about owning their own business?

It’s important to have enough money saved up to go through the beginning stages of starting a business. Make sure you have the cash to support your initial investment until your business is profitable.

Anything else you would like to share with other potential and actual small business owners?

If you are looking for an accounting plus cash flow management tool, you should try FINSYNC. The customer service is great, and they offer so many resources for your small business, such as financing. In my opinion, when looking for a tool, you need something user-friendly that’s really going to let you know what’s working and what’s not. Numbers tell a big story, and it’s better to have one tool like FINSYNC that helps you understand and move your business forward.

How FINSYNC Can Help

FINSYNC allows you to run your business on One Platform. You can send and receive payments, process payroll, automate accounting, and manage cash flow. To learn more about how we can help your business start, scale, and succeed, contact us today.